")

In the following weeks Klaveness Research will in a series of articles have a look at how we believe the fundamentals impacting dry bulk freight rates are shaping up for 2021.

In the first article we started off by having a look at the big picture. In the second, third, and fourth article we drilled further down into the details of the seaborne iron ore, coal and grains market. This week’s article will be on the minor bulks trade. In subsequent reports we will drill further down into the seaborne bauxite market before we finish off with a look at the supply side.

The link between the minor bulks trade and dry bulk freight rates

We include everything that is not iron ore, coal, grains or bauxite in the minor bulks group. The industry convention is to also include bauxite in the minor bulks group. However, as bauxite volumes and average distance traveled has increased rapidly in recent years, we believe it is long overdue to monitor bauxite on a standalone basis. Minor bulks had a 26%* market share in total dry bulk trade measured by volume in 2019 (left chart below). The demand for vessels cannot simply be derived from volume – we need to take distance and trade inefficiencies into account as well – as time spent on the total transport work is what ultimately impacts the aggregated demand for vessels. If we measure the share of minor bulks in total dry bulk trade by using the Dwt x Duration metric, we end up with a market share of 24% in 2019 (chart in the middle below), which is slightly lower than the volume based market share. In the first ten months of 2020 the market share of minor bulks has decreased one percentage point.

If we break it down by segment, we clearly see dominance of the geared vessels. 45% of all minor bulk volumes were carried on Supramaxes in 2019 (right chart above), followed by Handysize at 34% and short sea vessels at 12%. The market share of the Panamaxes segment is only 9% while the market share of Capesize vessels is virtually zero. If we pivot and instead look at the market share of minor bulks in each vessel segment’s carrying capacity, we see that minor bulks constitutes 78% of the demand for short sea vessels, 68% of the demand for Handysize vessels and 55% of the demand for Supramaxes (middle graph).

As minor bulks represent the lion’s share of the demand for geared vessels the link between the minor bulk trade and dry bulk freight rates in these segments is direct and clear. The minor bulk also impacts earnings in the Panamax and Capesize segments indirectly through substitution effects. Due to economies of scale the larger sizes can normally offer the cheapest freight on a per ton basis. When utilization is high in the Cape and Panamax segment it leads to higher freight rates which from time to time makes it cheaper to utilize geared vessels. The beneficiary of such cascading of volumes from the ungeared segments to the geared segments tend to be the Ultramaxes, the largest vessels within the Supramax segment. When the minor bulk volumes are high it increases the freight threshold where such cascading of volumes is triggered from the ungeared segment to the geared segments.

Minor Bulk Demand

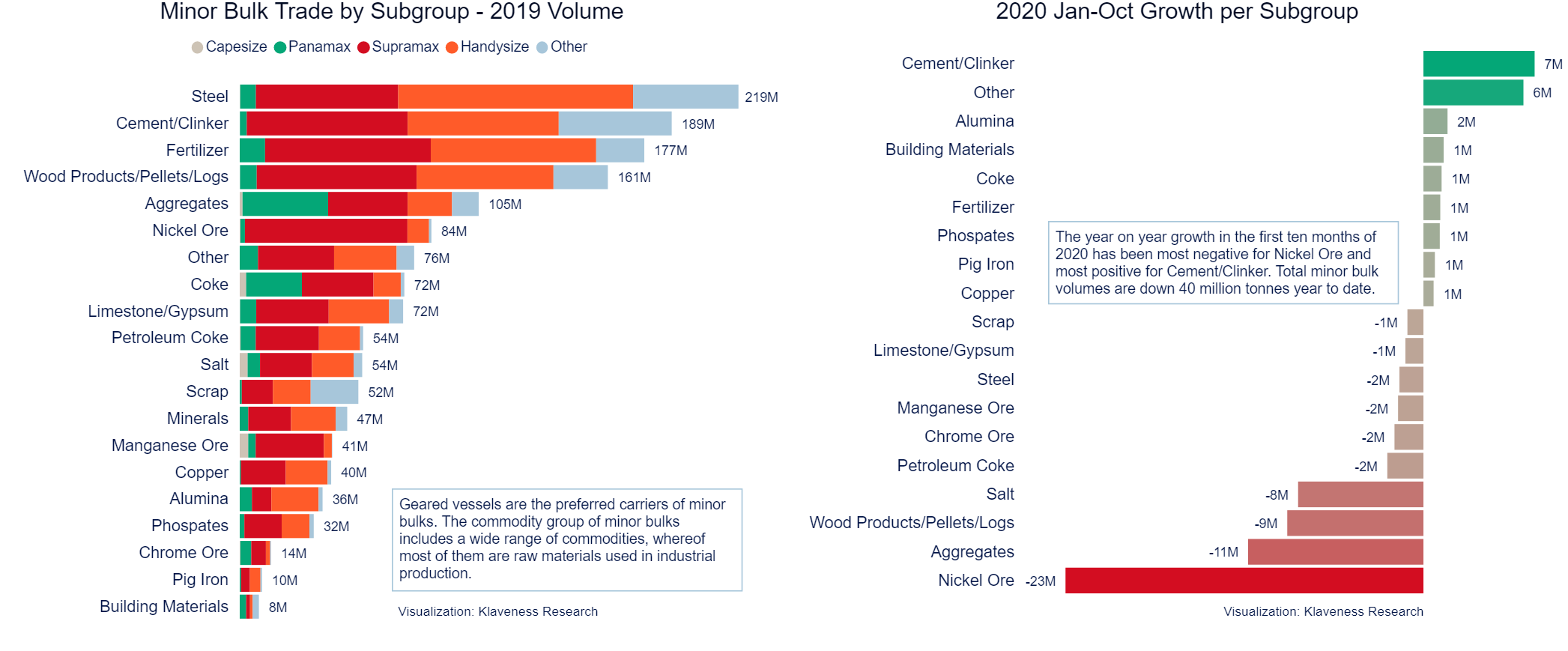

The commodity group of minor bulks includes a wide range of commodities, whereof most of them are raw materials used in industrial production. However, the largest subgroup is the semi finshed steel products which contains products such as steel slabs, rolled coils, pipes and billets. In 2019 the second largest sub group was the cement/clinker group, followed by fertilizers, wood products, aggregates and nickel ore.

Total minor bulk export volumes are down 40 million tonnes (-3.1%) in the first ten months of 2020 compared to the same period last year. This can broadly speaking be explained by two factors: the Indonesian ban on exports of nickel ore and decreasing global industrial production because of the Covid-19 epidemic.

Indonesian ban on export of nickel ore

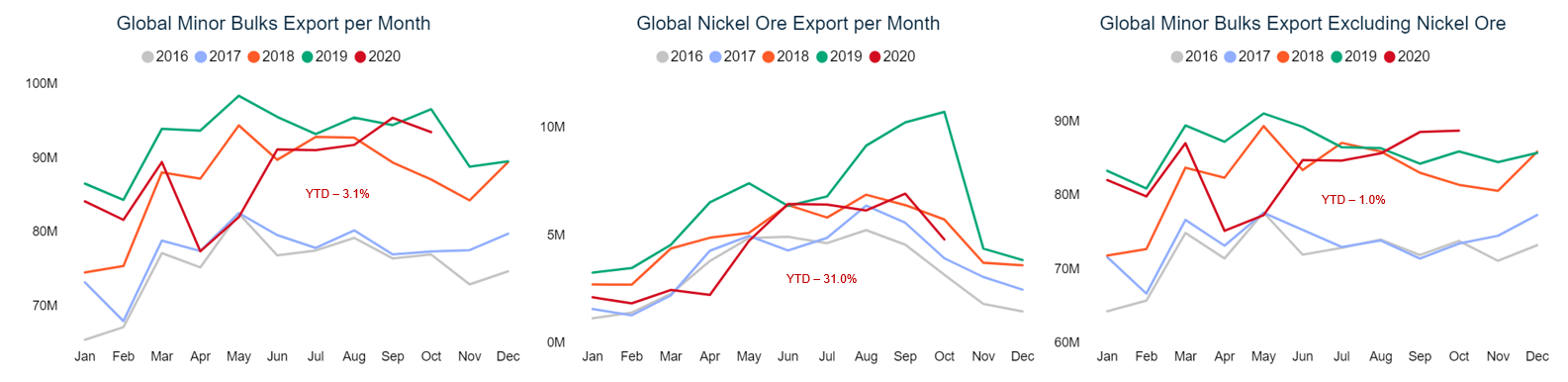

In recent years there have been three countries exporting nickel ore in substantial volumes. The Philippines has been the largest exporter with stable volumes while Indonesia ranks number two with huge swings in output from year to year. The last noteworthy exporting country is New Caledonia where volumes has been ramping up steadily. The graph on the left below shows total nickel ore export per country from 2013 to today.

Indonesia was the largest nickel ore exporter up until 2014 when a ban on the export of unprocessed minerals was introduced by the Indonesian government. The ban applied to other minerals as well, such as bauxite, but did not apply to coal. The motive behind the ban was to boost economic growth by promoting the development of a domestic processing industry. This led to very low export levels of these minerals between 2014 and 2016. In what has been commented on as a policy flip-flop, the ban was later relaxed in 2017 for those companies who had started the process of building refineries. This led to surging export volumes in 2018 and 2019 before the ban on nickel ore export once again was reinstated at the start of this year. As it looks now, we should not expect any sizeable nickel ore export out Indonesia in 2021. However, given the policy flip-flop seen in recent years it is not unlikely that some relaxation will occur in the future.

Global nickel ore export is down 31% year to date (see middle graph below) and this explains two thirds of the demand destruction we have seen in the minor bulk volumes in the first ten months of this year. About 80% of all nickel ore exports are destined for China. Nickel ore prices have been increasing in line with China’s recovering industrial production since April. On the back of increasing nickel prices we do expect the Philippines and other smaller exporters to increase their export somewhat in 2021, but it will not be anywhere close to offset the loss in volumes seen this year out of Indonesia. Nevertheless, the growth in nickel ore export will turn from sharply negative in 2020 to slightly positive in 2021.

The negative impact of Covid-19

Global minor bulk exports excluding nickel ore are down 1.0% year to date. This decrease can be attributed to the negative effect Covid-19 has had on global industrial production. Although we currently see a resurgence in global infections in the Western World we believe it is likely that the adverse effects from Covid-19 on global industrial production will be less in 2021 compared to this year. Either through vaccines or through increased knowledge about how to keep the wheels turning while at the same time keeping the virus under control. Thus, we expect global industrial production to stage a comeback in 2021. This is very likely to translate into higher demand for most of the minor bulks which again will have clear and direct positive effect on earnings in the geared segments. The graph on the right above shows that minor bulk export already is recovering and posted positive year on year growth in October. We expect the positive trend to continue into 2021 and we expect the magnitude of the growth to be negatively correlated with the growth rates in Covid-19 hospitalizations.

Next week we will take a closer look at how the fundamental drivers for bauxite is shaping up for 2021 before we finish up the series with a look on the supply side.

In the meantime, don’t hesitate to contact me if you have any questions regarding the content of this report or to discuss how we can help you manage your dry bulk exposure.

Source: Klaveness by Peter Lindström, Head of Research